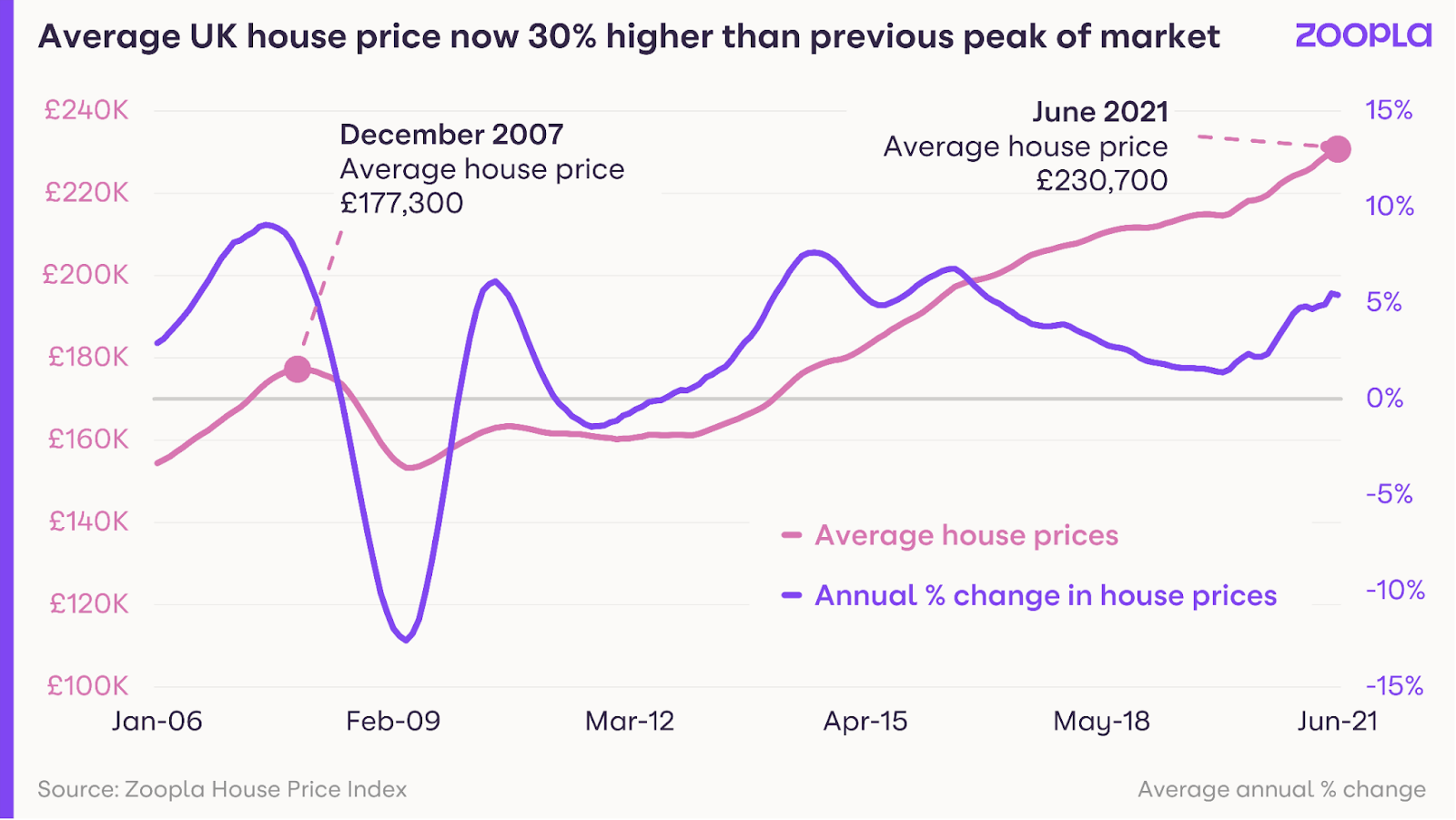

Average UK house prices reach new high of £230,700 - up 30% since 2007 market peak

27th July 2021

-

House price growth up +5.4% year on year in June, taking average house prices to a new high, some 30% above the 2007 market peak

-

House prices are being supported in part by a severe shortage of homes for sale, with stock levels down some -25% in the first half of the year compared to 2020

-

Sales agreed are running +22% ahead of average levels in 2020, but buyer demand fell 9% in the first half of June - albeit is still running +80% above the historic seasonal average

-

Demand for houses is twice as high as the 2017-2019 average, accelerating away from demand for flats, creating a disparity in average price growth across the two property types

-

Demand is also supporting property prices, with Northern Ireland and Wales registering the highest growth of +8.6% and +8.4% respectively - the highest growth for 16 years in Wales

-

London’s market is polarised, with demand in outer London running 86% ahead of the 2017-19 average, and demand in inner London running just 2% above the ‘normal’ market average

-

Price growth expected to edge upwards to 6% in the coming months before easing back to 4-5% towards the end of the year, as the impact of extended stamp duty unwinds

Tuesday 27th July, 2021, London: UK house prices have reached a new high, averaging £230,700 per property and now tracking 30% above the 2007 market peak. These are the latest insights from Zoopla, the UK’s leading property portal, in its monthly House Price Index.

House price growth continues to gather pace in post-pandemic windfall

House price growth was up +5.4% year on year in June, more than double the year on year price growth recorded 12 months ago, when annual house price inflation was tracking at +2.2%.

Pricing is being supported in part by a severe shortage of homes for sale. There has been a -25% fall in the volume of homes for sale in the first half of the year compared to the same period in 2020. Supply has now failed to keep pace with demand since January 2021, with no sign of a rebalance expected to play out imminently.

Transaction volumes also show no signs of abating, with sales agreed running 22% ahead of average levels in 2020. That said, buyer demand dipped 9% in the first half of July after the initial stamp duty holiday ended, but overall remains elevated - up +80% compared to the average for this time of year in the more ‘normal’ market conditions in 2017-19.

Demand is also supporting house price growth, with Northern Ireland and Wales registering the highest growth of +8.6% and +8.4% respectively, which equates to the highest growth in either country for 16 years in Wales.

At a regional level, house price growth is at its highest in the North West (+7.3%) and Yorkshire & the Humber (+6.8%), while London trails with annual house price growth of +2.3%.

Price growth is expected to edge upwards to 6% in the coming months before easing back towards the end of the year as the impact of the extended stamp duty holiday unwinds and the economic landscape becomes more challenging.

Figure 1

Demand for family houses up +114% compared to normal market conditions

Demand for all types of houses, from terraced to detached, has more than doubled, accelerating away from demand for flats, and creating a disparity in average price growth across the two property types.

Family homes are most popular amongst buyers, with demand up 114% compared to levels typically seen at this time of year between 2017-2019.

While flats and houses recorded almost equal price growth of +1.4% and +1.9% respectively in June 2020, the pandemic-borne ‘search for space’ has driven prices for houses up +7.3% over the past year.

By contrast, demand for flats has failed to keep pace and, as a result, prices growth is lagging at +1.4%, the same rate of growth seen last year.

Price growth for houses is highest in Wales at 10.2% and the North West at 8.8%, and weakest in London at +5.6%. Meanwhile, price growth for flats is highest in Scotland at 5.2% and East Midlands at 3.7% and weakest in London at -0.5%

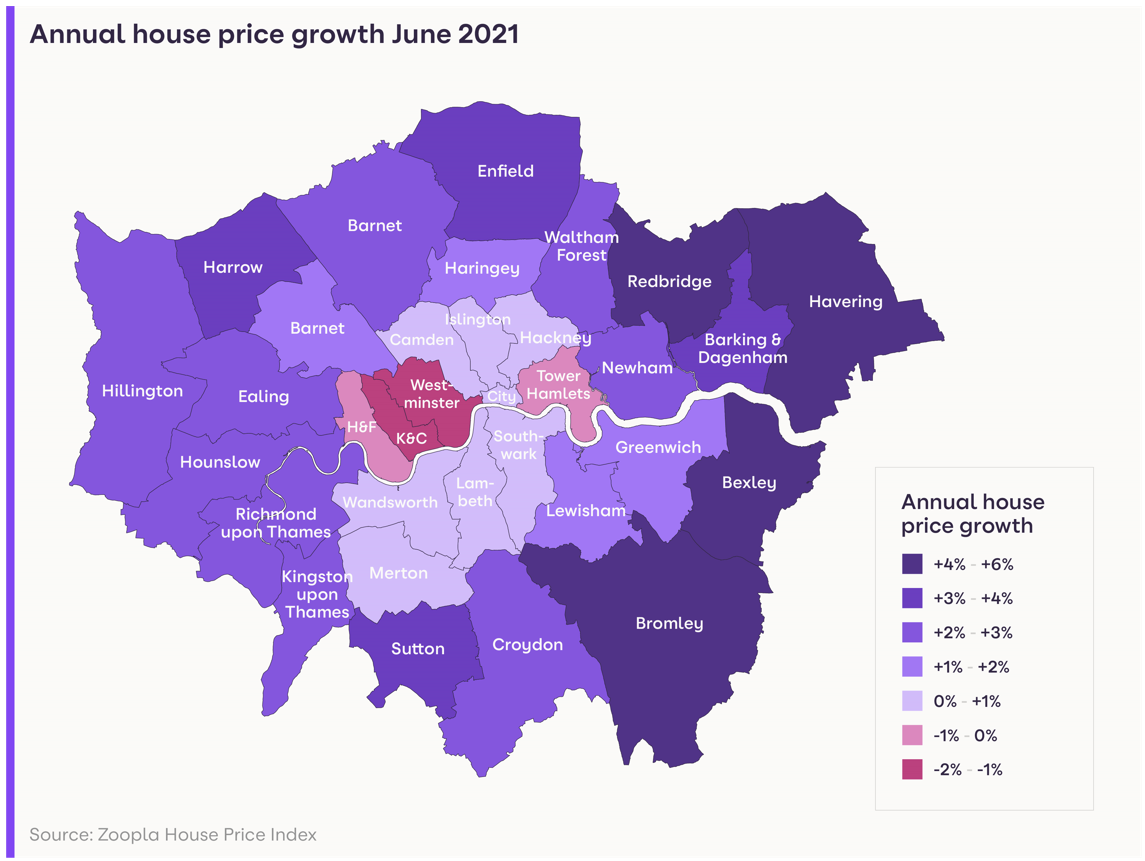

London market polarised

Annual price growth in London has been trailing the rest of the UK for eight months, and this month is no exception, with 2.3% growth, compared to an average of 5.4% across the country.

However, demand in London is polarised between inner and outer, with demand in outer London running 86% ahead of the 2017-19 average. This is explained in part by the available housing stock - with larger volumes of houses and properties with outside space

In contrast, demand in inner London is running just 2% above the ‘normal’ market average. This is also reflected in the pricing of properties, with London flats, predominantly clustered towards the centre, falling by 0.5% in the year to June, compared to houses, which have registered growth of +5.6%.

While inner London has been hampered by Covid, evidence suggests it could regain momentum providing there are no further pandemic setbacks. The rental market has already bounced back, and the sales market is set to follow given its proximity to offices and amenities.

Further relaxation on the restrictions around global travel will result in a firmer pick up in international demand, which would also reverse the downward trend in pricing - however a return to unrestricted international movement may be some way off.

Figure 2

Grainne Gilmore, Head of Research, Zoopla, comments: “Demand is moderating from record high levels earlier in the year, but remains significantly up from typical levels, signalling that above average activity levels will continue in the coming months.

“Demand for houses is still outstripping demand for flats. To a certain extent this trend will have been augmented by the stamp duty holiday, with bigger savings on offer for larger properties - typically houses. But underneath this, there is a continued drumbeat of demand for more space among buyers, both inside and outside, funnelling demand towards houses, resulting in stronger price growth for these properties..

”London has a two-speed market at present, with domestic demand driving price growth in the outer boroughs, while the lack of international business and leisure travel is affecting demand in the more global real estate markets towards the centre of London. As COVID progresses at different rates across the world, unrestricted travel may not resume for some time yet, but when it does, demand will start to pick up once more.

“Overall buyer demand coupled with constrained supply signal that price growth will continue to rise in the coming months, peaking at around 6%, before falling back to between 4%-5% by the end of 2021.”

- Ends -

For further information, please contact PR Team on pr@zoopla.co.uk or +44 (0)20 3873 8770.

About Zoopla

Hello. We're Zoopla. A property website and app.

We know you're not just looking for a place to live. You're looking for a home.

Yeah, we've got over a million properties for you to browse.

Tools that let you filter them in all kinds of clever ways.

And reliable house price estimates, so you can be sure you aren't paying over the odds.

But we know you're looking for more than that.

Because that first flat won't just be a 'great investment opportunity'.

It'll be the feeling of starting out on your own.

That extra bedroom won't just mean another £20K on the re-sale price, it'll mean having your sister over to stay.

And that bungalow won't just be a way to release some equity, it will be a chance to spend more time with the grandkids.

We know that searching for a home is about more than just checking its price, location and features (important as all those things are).

What really matters is how it makes you feel.

We know what a home is really worth.

So let us help you find yours.

Zoopla is part of Zoopla Limited which was founded in 2007.

Zoopla Limited, The Cooperage, 5 Copper Row, London, SE1 2LH

Registered in England and Wales with Company No. 06074771

VAT Registration number: 191 2231 33

Data Protection number: Z9972266