Houses for rent are letting 30% faster than a year ago pushing rents higher, but cities are feeling the brunt of the pandemic

9th February 2021

-

Once in a lifetime reassessment of housing needs reshapes the rental market in the wake of the pandemic

-

Easing demand in city centres means rents are falling in Edinburgh (-1.8%), Greater Manchester (-0.9%) and Greater Birmingham (-0.8%)

-

But a halo effect has emerged as rents rise strongly across the wider commuter zones of the UK’s largest cities, driven by rising demand among renters migrating towards more space

-

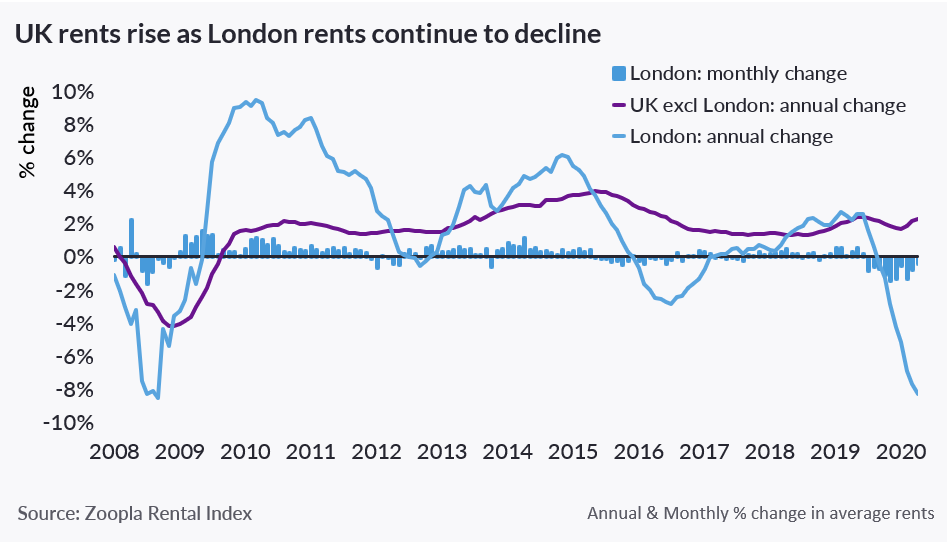

London’s position as a global city means current rental trends have been amplified, with rents registering the steepest annual fall (-8.3%) since the Global Financial Crisis

-

However, the downturn in London rents is starting to ease - signalled by the monthly decline in December, which, at -0.4%, was the most modest monthly fall since pre-pandemic

-

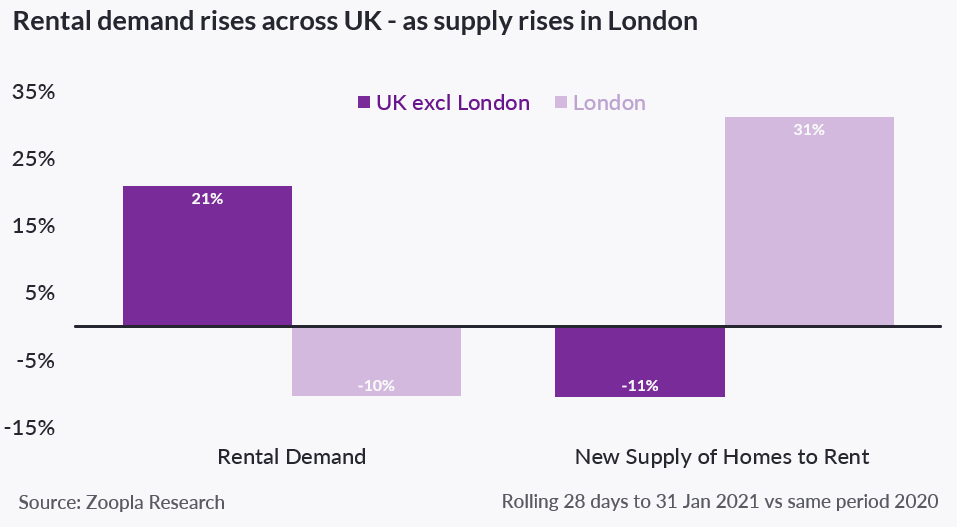

Across the UK as a whole, excluding London, rents are running at +2.3%, matching pre-Covid levels, and demand is up 21% year on year*

-

Market outlook depends on how quickly the vaccine can reduce the impact of Covid and when business as usual resumes in city centres

-

Flexible working is likely to result in a permanent shift in priorities for some renters, while the demand for space is likely to hold firm, supporting the family homes rental market

Tuesday 9th February 2021, London: The pandemic continues to shape the UK property market, with the effects felt most acutely in the growing disparity between inner city and outer city residential rents. These are the latest findings by Zoopla, the UK’s leading property portal, in its quarterly Rental Market Report.

Rents diverge across inner and outer city markets

Changing patterns in working and commuting, leisure and tourism, have eased rental demand in city centres across the UK, with an annual fall in rents that began before the onslaught of the pandemic in Edinburgh (-1.8%), Greater Manchester (-0.9%) and Greater Birmingham (-0.8%).

By contrast, a halo effect has emerged in the wider commuter zones of the UK’s largest cities. Rents are rising strongly in the wake of increased demand among some renters who are migrating towards properties with more space, indoors and outdoors, as a result of three successive lockdowns over the past 10 months.

Pockets of demand and rental performance have been redefined across inner and outer cities. For example, rents in central Birmingham fell by -3.4% in the year to December, but in the surrounding boroughs of Bromsgrove, Sandwell and Wolverhampton, rents rose by an average of 5%.

Rents in well-connected towns are also registering strong growth (Rochdale +8.2%, Hastings +8.0%, Southend +5.8% and Newport in Wales +5.5%), with demand buoyed by renters freed from the daily commute, and reprioritising their housing needs and location.

Across the UK as a whole, excluding London, rents are running at +2.3%, matching pre-Covid levels, and demand is up 21% year on year* [see figure 1].

Figure 1:

Figure 2:

Covid impact amplified in London

London’s position as a global city means current rental trends have been amplified. Demand in London is down 10% year on year in January, resulting from the triple impact of working from home policies, reduced international travel, and a near cessation of tourism. In addition, Greater London rents have registered the steepest annual fall (-8.3%) since the Global Financial Crisis.

The fall in overall average rents is being exaggerated by declines in the higher value, more dense rental markets of inner London and Kensington & Chelsea (-12.3%). However, while rents are falling by at least 6% in most inner London boroughs, several outer London boroughs are still showing rental growth (Havering +2.6% and Enfield +1.1%). Furthermore, the downturn in London rents is starting to ease - signalled by the monthly decline in December, which, at -0.4%, was the most modest monthly fall since February 2020.

New supply in London is up 30% year on year as short-lets continue to be transitioned into long-lets, and more new build rental supply comes to market, creating more choice for renters and exerting downward pressure on rents.

Higher levels of stock availability are expected to characterise the London market over the course of 2021, pending a post-Covid return to international travel, commuting, employment growth and offices opening at scale.

Space race extends to rentals

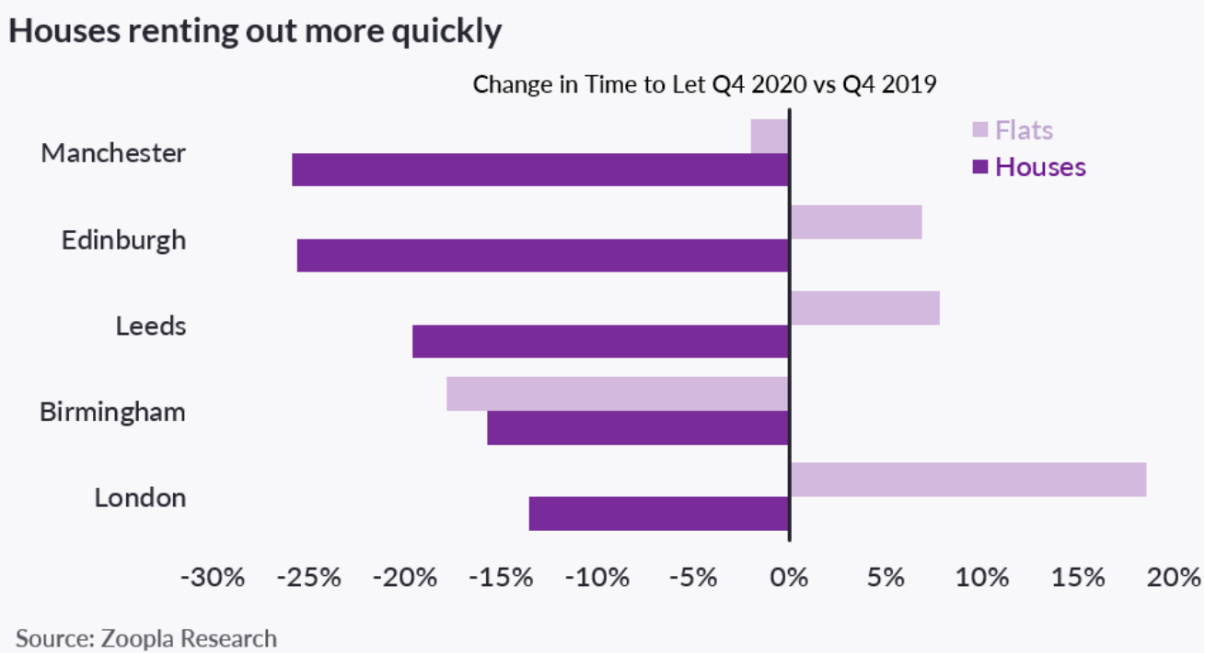

As Covid stimulates ongoing demand for more space, replicating the trend seen in the sales market, houses are now renting out more quickly than a year ago in most key cities (London, Leeds, Edinburgh, Manchester and Birmingham), while in some cases flats are spending longer on the rental market before being snapped up (see figure 3). From a UK perspective, it's taking 30% less time to rent out a house and 2% less time to rent out a flat.

In Leeds, it took 20% less time to rent out a house in Q4 2020 compared to the previous year, whereas it’s taking 8% longer to rent out a flat; meanwhile in London, it’s now 14% faster to rent out a house, while it’s taking 19% longer to rent out a flat.

In Manchester, it’s now quicker to rent out a house (14 days) than a flat (16 days) - a reversal from Q4 2019, when it generally took three days longer to rent out a house than a flat.

With renters moving to where they can access more space affordably, and with more houses typically located outside of city centres, this is also contributing to the halo effect of increased demand and rental growth in our city markets and the widest points within a commuter zone.

As a result of changing demand patterns, in every region of the country, a larger proportion of rental flats than houses are having their asking rents reduced in a bid to attract tenants.

Figure 3

Looking ahead to the rest of the year

Demand in the rental market is driven by labour mobility, migration and employment growth, all of which have been disrupted by the pandemic.

The outlook for the rental market depends upon how quickly the roll out of the vaccine can reduce the impact of Covid and, in turn, when business as usual resumes in city centres, with the reopening of shops and offices, leisure and entertainment facilities, and a return to more business activity.

Flexible working is likely to continue, meaning there may be a permanent shift in priorities for some renters. The demand for space is unlikely to diminish any time soon, which will continue to support the family homes rental market.

Overall, Covid-led uncertainty, rising unemployment and a lack of mortgage availability at high loan-to-values will lead to sustained demand in the rental sector. At the same time, a lack of new investment in rented homes by private landlords since 2016 means the supply of homes for rent is not rising nationally and this will also support rental growth in the long run.

Grainne Gilmore, head of research, Zoopla, comments: “Changing working, commuting and tourism patterns were felt very quickly in the central London rental market. Now we are seeing the impact in other city centres, although on a more modest scale. Balancing the rental declines in inner cities is the strong rise in rental growth in surrounding ‘halo’ areas and well-connected towns across the UK, reflecting stronger demand in many of these markets among a cohort of renters. Yet it is important to note that most demand among renters living in central cities is within the same area - some renters will have ties to an area through schooling, or non-office based work.

“The search for space among renters is coming across loud and clear from the data however, with houses in major cities now being rented out more quickly than a year ago. In most cases, flats are now taking longer to rent out.”

*UK excluding London year on year growth - rolling 28 days to 31/01/2021 versus the previous year

- Ends -

For further information, please contact PR Team on pr@zoopla.co.uk or +44 (0)20 3873 8770.

About Zoopla

Hello. We're Zoopla. A property website and app.

We know you're not just looking for a place to live. You're looking for a home.

Yeah, we've got over a million properties for you to browse.

Tools that let you filter them in all kinds of clever ways.

And reliable house price estimates, so you can be sure you aren't paying over the odds.

But we know you're looking for more than that.

Because that first flat won't just be a 'great investment opportunity'.

It'll be the feeling of starting out on your own.

That extra bedroom won't just mean another £20K on the re-sale price, it'll mean having your sister over to stay.

And that bungalow won't just be a way to release some equity, it will be a chance to spend more time with the grandkids.

We know that searching for a home is about more than just checking its price, location and features (important as all those things are).

What really matters is how it makes you feel.

We know what a home is really worth.

So let us help you find yours.

Zoopla is part of Zoopla Limited which was founded in 2007.

Zoopla Limited, The Cooperage, 5 Copper Row, London, SE1 2LH

Registered in England and Wales with Company No. 06074771

VAT Registration number: 191 2231 33

Data Protection number: Z9972266