HOUSING SALES LAG 20% BEHIND 2019 AS MARKET LOSES 124,000 SALES WORTH £27BN DUE TO LOCKDOWN

28th July 2020

-

New sales agreed are running 28% above pre-lockdown levels as the surge in demand converts into actual sales

-

The market continues to play ‘catch-up’, with sales agreed, since the start of 2020, 20% below the same period in 2019 - amounting to 124,000 lost sales worth £27bn since March

-

Housing sales across whole of 2020 expected to be 15% lower than 2019 as a result of COVID

-

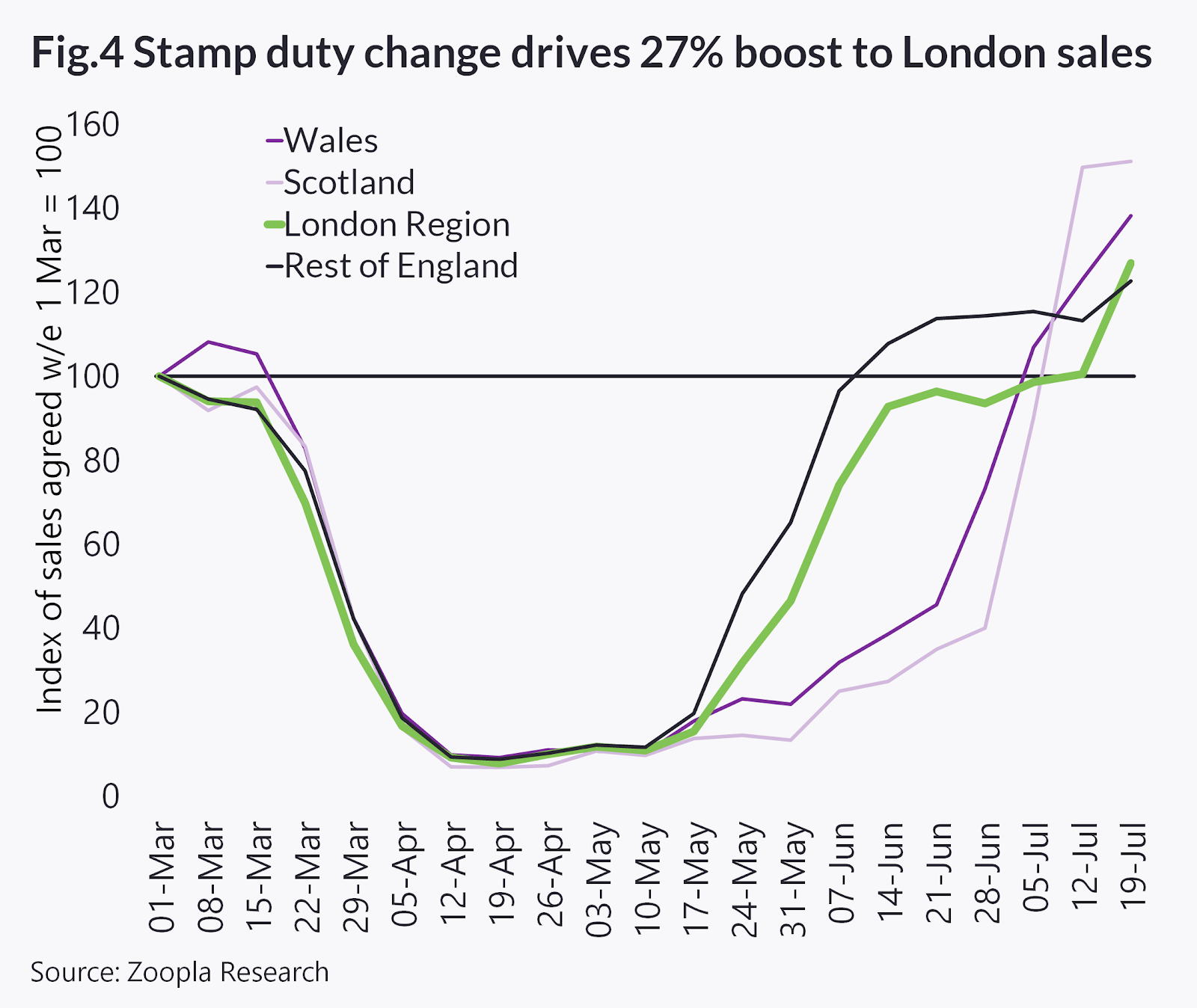

Stamp duty changes have driven a 27% increase in sales agreed in London over the last two weeks, but have had less impact on sales in regional housing markets across England

-

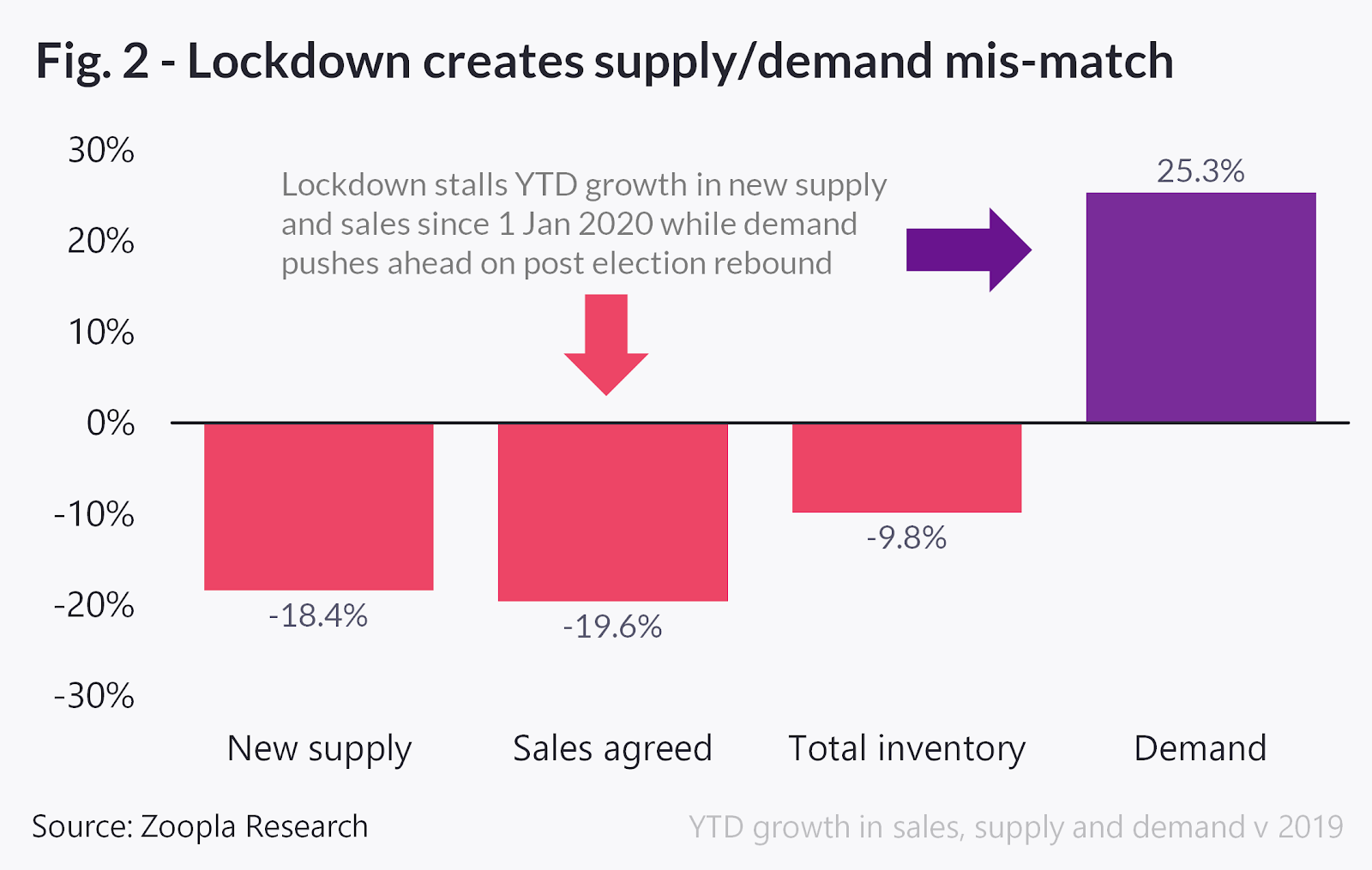

The lockdown has created a supply/demand imbalance. While sales are behind last year, the growth in demand over 2020 is ahead of last year by 25% thanks to the strong start to the year and the scale of the post COVID rebound

-

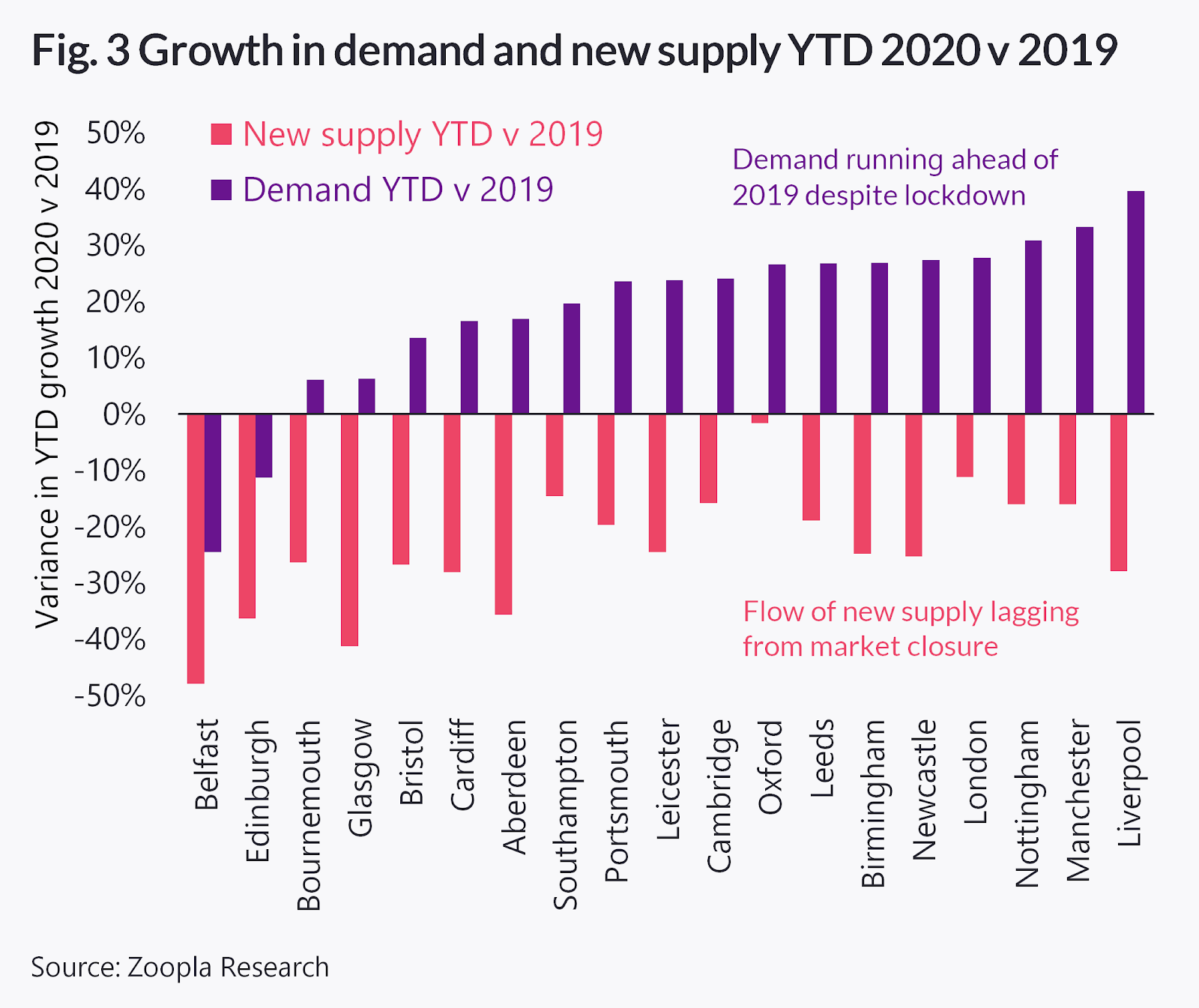

The supply/demand imbalance is greatest in northern cities such as Sheffield, Liverpool and Manchester where house price growth is above average

-

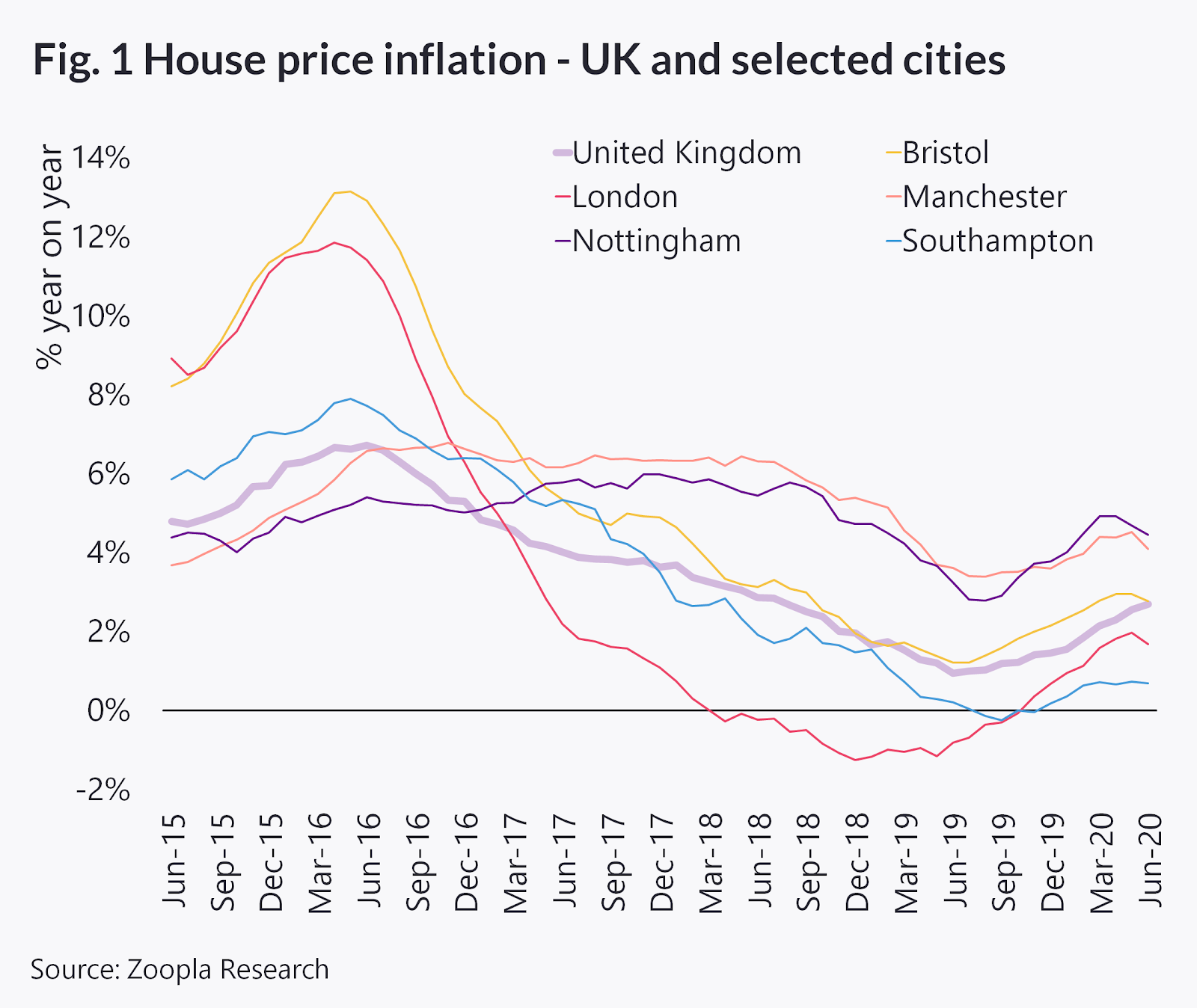

Zoopla’s UK house price index is registering annual growth of +2.7% as the strong start of 2020 supports the headline rate of growth - the monthly rate of growth has halved to 0.2%

Tuesday 28th July 2020, London: The property market is set to lose 124,000 sales in 2020, with a combined value of £27bn, as a result of the COVID market suspension. These are the latest findings in the monthly House Price Index by Zoopla, the UK’s leading property destination.

124,000 lost sales

Sales volumes are expected to be the greatest casualty of the market closure. After the strongest start to the year for five years, completed sales between the start of January and the end of June are lagging 20% behind 2019 across the same period. This equates to some 124,000 lost sales, despite record levels of demand for housing over recent weeks.

By the end of the year, the lag is expected to have made a marginal recovery, with total transaction volumes for 2020 netting out at 15% below 2019.

A supply and demand imbalance

The dynamics of housing supply and demand have been heavily impacted by lockdown and the 50 day market closure in England. The market suspension reduced the flow of new supply and sales agreed by 90%. While these measures are now rising ahead of their pre COVID levels, the increase in sales and supply since the start of the year is still lagging 20% behind compared to 2019. Overall, stock levels are running at 10% below this time a year ago [see figure 2].

In contrast, demand for housing has rebounded strongly as pent-up demand returns to the market. In the last month demand from buyers has been twice the same period in 2019. On a cumulative basis, since January 2020, demand is running 25% higher than the same period in 2019 despite the lockdown and market closure.

Our analysis shows this is primarily ‘catch-up’ demand for what was lost over lockdown, and it’s estimated that returning buyers account for 80% of levels that would have been expected over this period in 2020 had COVID not struck.

Looking at trends since the start of the year, it is clear there is a widening gap between supply and demand. This is expected to support house prices over the second half of 2020 with year on year declines in capital values unlikely before the year end.

Regional cities across the north of England have recorded stronger growth in demand in the first half of 2020 compared to 2019, while new supply has been hit country-wide as a result of the market closure [see figure 3]. The greatest short-term support for prices will be in cities where demand has grown the most over the first seven months of 2020 compared to 2019 - top of the list for demand are Sheffield, Liverpool, Manchester and Nottingham, which are all in the top five fastest growing cities in terms of house price growth.

Flight from cities is overstated

Short-term demand for city living is holding firm, but there has been much speculation about the long-term demand for city homes. Research suggests that COVID boosted demand for homes outside major cities; however, we expect this to be a one-off factor rather than a long-term ‘seismic shift’ in consumer attitudes.

London ranks fifth for growth in demand since the start of 2020 [see figure 3] and, when we examine it by inner, outer and commuter areas, we can see that demand has seen a modest shift away from the centre, towards the suburbs and commuter belt. The lockdown has changed the priorities of today’s buyers who want a garden and are planning to commute less. This means consumers will look where this type of housing is available and meets their budget, which for many is outside inner London.

We see this as a shift in consumer focus rather than a structural change in market fundamentals. As cities start to re-open, we expect some rebalancing in between demand for homes in higher density areas of cities and their suburbs and commuter hinterlands.

A stamp duty bias

Despite an overall decline in annual transactions, London enjoyed an immediate boost to sales agreed following the stamp duty holiday recently announced in the Summer Statement.

New sales agreed have increased by over a quarter (27%) in just two weeks in London, which was geared to benefit most from the changes [see figure 4].

This boost to transaction volumes has not been replicated in other regions, where average property prices are lower and less responsive to stamp duty amends. While stamp duty relief will support demand in higher value markets [on property priced up to £500,00] across southern England, it is unlikely to sustain demand indefinitely into 2021.

Outlook for pricing - what’s next?

At present, UK house price inflation in the 12 months to June 2020 have edged up to +2.7%, registering the highest level of annual growth for almost two years. By contrast, the monthly rate of growth has halved to 0.2% and the city level price indices are registering slower growth still as a result of lockdown and reduced pricing evidence.

While there is a wide variation in annual growth rates across the country, there is no evidence of material, localised annual price falls at a regional or city level.

Based on current trends, the headline annual rate of growth is set to remain positive, as the growing imbalance of supply and demand is set to support prices for the remainder of the year.

Commenting on the latest UK House Price Index, Richard Donnell, Research and Insight Director, Zoopla, said: “COVID and the lockdown have shifted the dynamics of supply and demand across the housing market. The staggered reopening of housing markets across countries and the added impetus from the stamp duty holiday mean we expect buyer demand and new sales volumes to hold at current levels over the next two months. The net result will be continued support for house price growth at current levels over the second half of the year. Regional cities in northern England and the Midlands have the strongest underlying trends.

“For those operating in the market, and others looking in, the latest forecasts for increased unemployment and a sharp economic contraction over the next 12-18 months certainly seem at odds with current levels of sales market activity.

“We expect rising unemployment to weigh on market activity over the final quarter of 2020 and into the first half of 2021. The impact on pricing looks set to be pushed into 2021 as a result of sizable Government support for the economy. Further support cannot be ruled out while forbearance by lenders, and the availability of the mortgage payment deferrals, which can start up until the end of October for 3-6 months, is likely to limit the scale of downside for house prices. Much depends on how businesses respond to the outlook and their decisions on staffing levels and the knock on impact for unemployment.”

- Ends -

For further information, please contact PR Team on pr@zoopla.co.uk or +44 (0)20 3873 8770.

About Zoopla

Hello. We're Zoopla. A property website and app.

We know you're not just looking for a place to live. You're looking for a home.

Yeah, we've got over a million properties for you to browse.

Tools that let you filter them in all kinds of clever ways.

And reliable house price estimates, so you can be sure you aren't paying over the odds.

But we know you're looking for more than that.

Because that first flat won't just be a 'great investment opportunity'.

It'll be the feeling of starting out on your own.

That extra bedroom won't just mean another £20K on the re-sale price, it'll mean having your sister over to stay.

And that bungalow won't just be a way to release some equity, it will be a chance to spend more time with the grandkids.

We know that searching for a home is about more than just checking its price, location and features (important as all those things are).

What really matters is how it makes you feel.

We know what a home is really worth.

So let us help you find yours.

Zoopla is part of Zoopla Limited which was founded in 2007.

Zoopla Limited, The Cooperage, 5 Copper Row, London, SE1 2LH

Registered in England and Wales with Company No. 06074771

VAT Registration number: 191 2231 33

Data Protection number: Z9972266