Rental growth in London tumbles in response to COVID-19, while Zoopla expects rental growth outside London to halve to +1% by the end of the year

5th August 2020

-

A two-speed rental market is emerging in the UK, driven by divergent trends in supply and demand between London and the rest of the country

-

Rents in London have fallen 3% since the start of the year and are down by 1.4% over the last 12 months

-

Inner London seeing the greatest downward pressure on rents as the working-from-home policy and reduced international travel and tourism impact the pool of demand for rented property, while available supply has increased

-

Rental growth across the regions and countries excluding London remains positive - from 1.5% in the West Midlands to 3.1% in Wales - supported by pent up demand for rented housing

-

Edinburgh - the second most popular tourist destination in the UK - has seen a sharp slowdown in rental growth linked to a shift in short to long term rents and policy changes

-

Zoopla Research expects annual rental growth in the UK outside London to slow from +2.2% today to +1% by the end of the year, with an annual decline in London of up to -5% by the end of 2020

Wednesday 5th August, 2020; London: Average rents across the UK dipped by -0.3% in June, and by -0.8% in Q2, taking the annual growth in UK rents to +1.1%, down from +1.7% a year ago. However, a two-speed market has emerged between London and the rest of the UK. These are the latest findings of the quarterly Rental Market Report by Zoopla - the UK’s leading property resource.

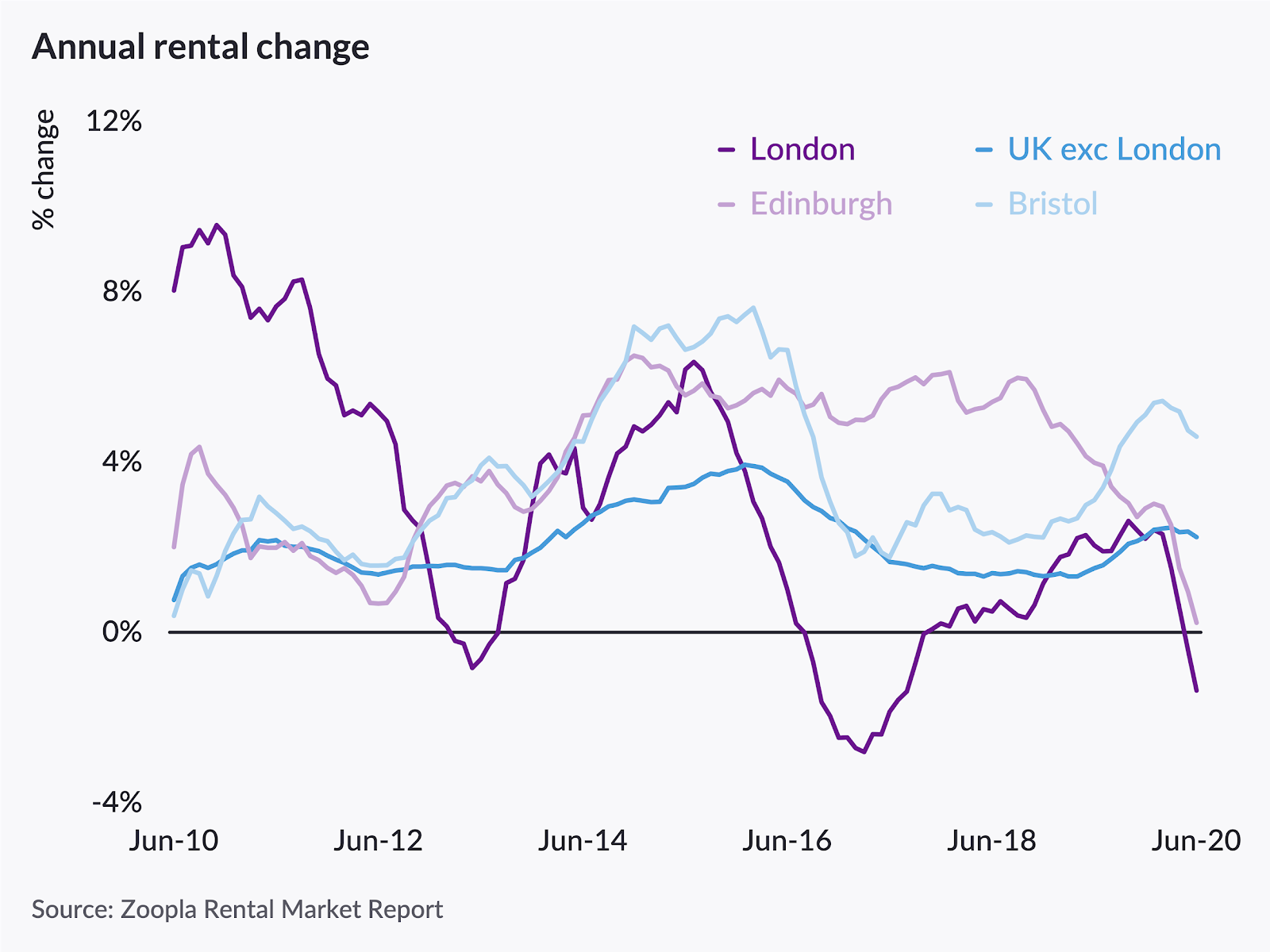

Figure 1:

A two-speed market

Rental growth in the UK excluding London is up +2.2%, as demand continues to outstrip supply in many markets. By contrast, a different trend is emerging in London, with rising supply and weaker demand - particularly in inner London - resulting in negative rental growth. Edinburgh has also seen a marked slowdown in rental growth to +0.2% over the past year as a result of reduced tourism and policy changes impacting landlords and the supply of property.

Challenging market conditions in London and Edinburgh

The rental markets of London and Edinburgh stand apart from other UK cities in the UK; a rise in supply in these markets, which is increasing choice for renters, is not being matched by similar levels of demand, leading to downward pressure on rents and the rate of rental growth.

Several Covid-related factors have resulted in rising supply in London - in particular in central and inner zones.

The decline in international travel and tourism has seen landlords in the capital, especially in central London, shifting away from short lets, thereby increasing supply in the long let market. Weaker demand means that as tenancies end, they are being absorbed more slowly, compounding the growth in supply.

The rise of homeworking at many firms, with a slow return to offices over the rest of the year, signal that demand for rental property is likely to remain subdued, especially if unemployment starts to rise. Commuting data shows that working patterns in London are still far from returning to levels seen back in March.

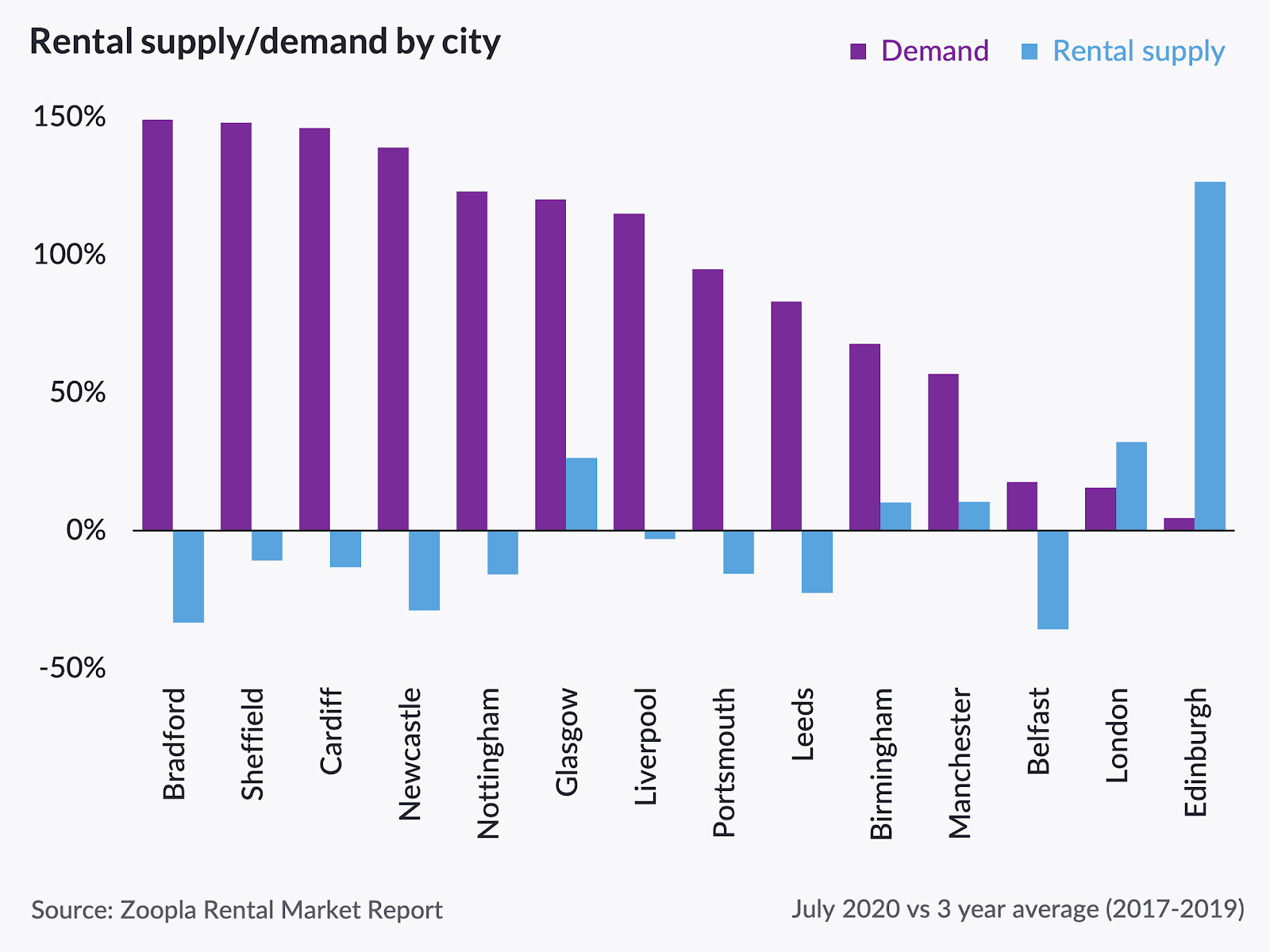

Figure 2:

In addition, the student influx expected as part of the usual seasonal busy period in late summer may not be as large this year, as universities migrate towards more online learning.

There is not a one-size fits all picture in London, however. The factors above are most pronounced in central and inner London, where rents are generally higher, and less business travel and business-related rentals with reduced tourism are impacting demand.

Average rents in London have fallen by -3% over 2020 H1 and are down 1.4% on the year. This is the second time rents have fallen into negative territory in the last three years in the capital - rents fell to -2.8% in March 2017 on the back of rising supply after the introduction of the additional 3% stamp duty change in 2016.

In Edinburgh, where annual rental growth has slowed to +0.2%, down from +4% a year ago, the rise in supply has also been exacerbated from the movement into the mainstream rental market by landlords who had been operating their properties as short lets.

The uncertain outlook for international tourism, as well as new legislation that may limit the types of homes that can be used for short lets in the Scottish capital, is likely to have created a one-off shift in properties to mainstream rental.

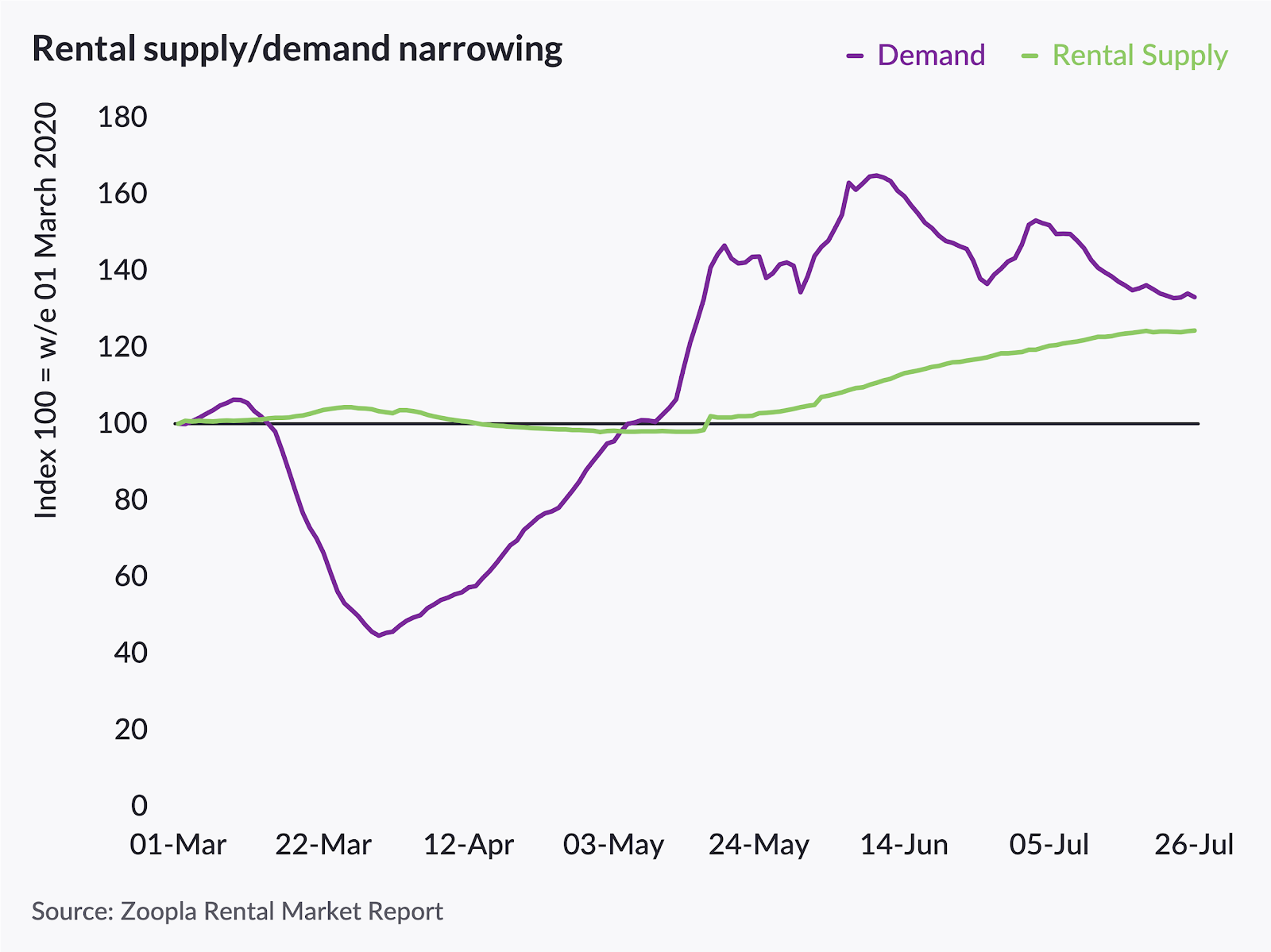

A rebound in demand elsewhere

Rental demand was more resilient during lockdown than demand in the sales market, and although levels are starting to moderate, they are running 33% higher than pre-lockdown, and 25% above 2019 levels across the UK as pent-up demand comes back to the market. Renters, like homeowners, may have used lockdown as a chance to reassess how and where they are living, further boosting rental market activity.

At the same time, the number of homes for rent has increased since lockdown ended - and is slightly ahead of seasonal trends, with the volume of homes for rent nationally up 7% on this time last year.

As this gap between demand and supply continues to narrow through Q3 and Q4, rental growth will start to slow as tenants benefit from a wider array of properties to choose from.

Figure 3:

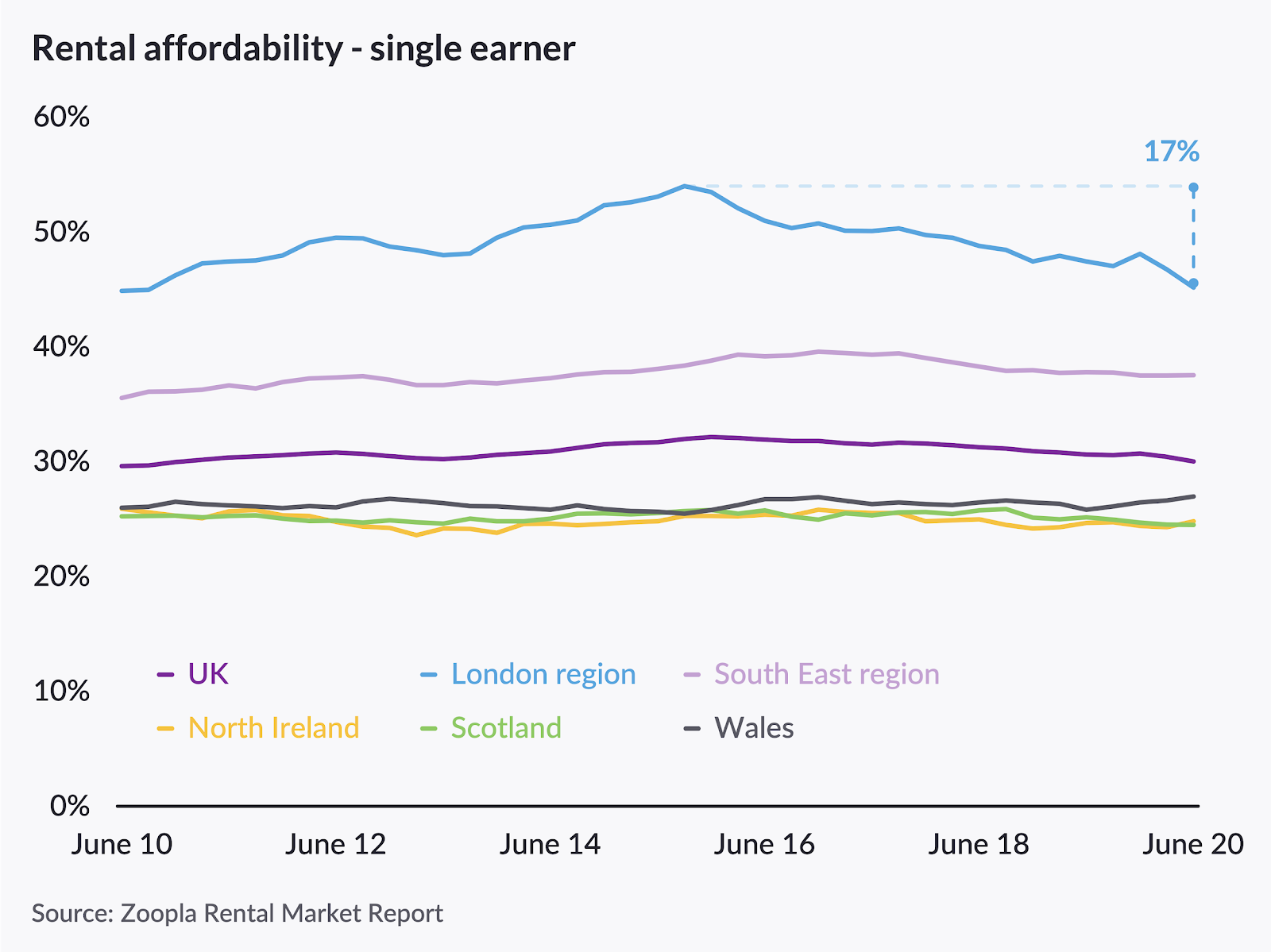

Steady levels of affordability

Levels of affordability within the rental sector have remained largely unchanged in recent years, with the exception of London, where the proportion of income needed to cover average monthly rent has fallen to 45% from 54% in September 2014, although it still remains the most expensive region in the UK in which to rent a home.

Figure 4:

Commenting on the latest Rental Market Report by Zoopla, Gráinne Gilmore, Head of Research, said: “The future path of annual rental growth will be determined largely by the economic outlook,

especially the rise in unemployment and the future path of average earnings. However, as new rental

supply continues to catch up with demand levels, we could see further softening of headline rental

growth by the end of the year, although there will be some areas of outperformance.

“Uncertainty continues over how any further outbreaks of COVID will impact the resumption of office life, student life and tourism, and this uncertainty will impact demand in some markets during the rest of the year.”

- Ends -

For further information, please contact PR Team on pr@zoopla.co.uk or +44 (0)20 3873 8770.

About Zoopla

Hello. We're Zoopla. A property website and app.

We know you're not just looking for a place to live. You're looking for a home.

Yeah, we've got over a million properties for you to browse.

Tools that let you filter them in all kinds of clever ways.

And reliable house price estimates, so you can be sure you aren't paying over the odds.

But we know you're looking for more than that.

Because that first flat won't just be a 'great investment opportunity'.

It'll be the feeling of starting out on your own.

That extra bedroom won't just mean another £20K on the re-sale price, it'll mean having your sister over to stay.

And that bungalow won't just be a way to release some equity, it will be a chance to spend more time with the grandkids.

We know that searching for a home is about more than just checking its price, location and features (important as all those things are).

What really matters is how it makes you feel.

We know what a home is really worth.

So let us help you find yours.

Zoopla is part of Zoopla Limited which was founded in 2007.

Zoopla Limited, The Cooperage, 5 Copper Row, London, SE1 2LH

Registered in England and Wales with Company No. 06074771

VAT Registration number: 191 2231 33

Data Protection number: Z9972266